Desperate RBM issues securities at 40%

In a desperate attempt to control money supply and rein in inflation, the Reserve Bank of Malawi (RBM) has issued securities—tradable instruments—worth K17.9 billion at over 40 percent, a move condemned by an  economist as counterproductive.

economist as counterproductive.

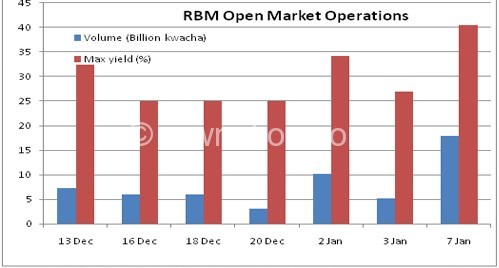

According RBM daily money market reports, the central bank has issued securities through Open Market Operations (OMO)—the buying and selling of government securities in an open market to expand or contract money supply—at a rate up to 40 percent, which is 15 percentage points above the bank rate at 25 percent.

Currently, inflation, the rate at which the general level of prices for goods and services is rising, is at 22.9 percent as of November 2013, according to the National Statistical Office (NSO), casting doubt on government meeting its annual projection.

Chancellor College economics professor Ben Kaluwa in an interview on Wednesday said the central bank is desperate to control money supply and control inflation, but was quick to point out that the policy is wrong.

“The RBM is obsessed with controlling money supply to control inflation. This is a wrong approach in Malawi. The central bank is using wrong instruments for a good cause. We all know that inflation is mainly influenced by food prices and so why not target an increase in its production which will lead to lower prices?

He said the monetary policy that the RBM is using is applicable in developed economies where inflation rates are below five percent.

Kaluwa warned that the move may lead to a further rise in interest rates because all yields for securities influence interest rates.

He argued that the situation will encourage commercial banks to buy the securities and not lend to businesses, hence denying resources to businesses.

End-March 2013, interest rates jumped to over 40 percent in response to yields for Treasury Bills (T-bills) that rose to around 43 percent.

This year, commercial banks have started increasing their lending rates to around 40 percent in the wake of a Lombard facility pegged at 27 percent, a situation that will have dire implications for businesses and consumers who want to borrow or service loans.

On January 2, according to RBM money market reports, the central bank issued securities valued at K10.2 billion through OMO at an average 27.6 percent.

Only “political will” can bring about financial reform in Malawi to reduce lending rates. Banks cannot self-regulate because past statistics on which they base decisions for non-performing loans ( a fancy word for defaulted loans) would show high past failure rate. The high failure rate was because of the high interest rates (40%) – a vicious cycle. Any risk analysis models, based on this historical data therefore, cannot be used to trigger lending rate cuts. Malawi needs political will to intervene and cut lending rates!

Regarding the securities sell, it must be looked at holistically. It appears this move is aimed at influencing the activities of the banks. This is not a ‘money supply’ issue as has been stated in the article but this is a ‘monetary base’ issue. Monetary base being high-powered money because it has quick impact on money multiplier in Malawi economy so the move is more intended to influence bank behaviour and to shrink credit in the economy, it appears to me.

Fighting inflation in Malawi is all left to RBM alone, which is not right. Monetary policy must be supplemented by Fiscal policy from Ministry of Finance. The Ministry of Finance must look at things like i) food availability to counter food driven component of the inflation ii) selective use of duty and tariffs to counter imports of certain high inflationary commodities, if need be ii) stop importing certain items. This is where I say monetary policy and fiscal policy are not working in perfect harmony to supplement each other effort. RBM can only use monetary policy to combat inflation while the rest must be done by Finance ministry. The action taken here is std reserve banks practice world over given that as of 10 Jan 2014 the banking sector in Malawi had excess reserves of K25bn over and above the K43bn LRR at 15.5% target. Therefore, whereas at micro level the move is justifiable as a normal course of action in managing monetary policy but at strategic level it does not promote job creation. That is the heart of the problem for Malawi.

That is why Malawi must first define development/economic growth policy goals to emphasize job creation, economic growth and price stability. Reform monetary policy with a goal of driving lending rates to below 10% to support govt stated job creation goals. Finance ministry fiscal policy must coordinate it all to orchestrate moving the country to the next level of development.