Firms’ bad loans provision down

Provision for bad loans for private sector credit has declined by 0.5 percentage points in the first half of this year, a situation market analysts say indicates a positive outlook for investments.

Provision for bad loans or a loan loss provision is an income expense set aside to allow for uncollected loans and loan payments.

In an interview on Tuesday, market analyst Cosmas Chigwe said the development could be attributed to the fact that many banks are restructuring their asset books.

He said: “Rates below five percent are actually a positive trend sign in general. Over the last few years, the central bank’s management of how banks treat their loan books has commendably improved tenfold.

“It should be noted that it is the treatment of loans by banks that has changed. This could mean a lot of banks are simply restructuring their asset books to manage reported losses.”

But Chigwe said this does not indicate an improvement in loan repayment culture in the country.

Figures from the Reserve Bank of Malawi (RBM) show that provisional losses for private sector credit averaged negative 4.9 percent in the past year, declining from negative 4.4 percent in June 2020 to negative 4.1 percent in June 2021.

During the review period, the community, social and personal services sector private sector loans have taken the largest share of credit at 29.1 percent of sectoral loan distribution from 14.8 percent.

Wholesale and retail trade (23.2 percent), agriculture, forestry, fishing and hunting (18.1) and manufacturing (13.5) have seen their private sector shares drop from 23.6 percent, 20.8 percent and 15.9 percent, from June 2020 to June 2021 in that order.

In a separate interview, economist Bond Mtembezeka, who is also Alliance Capital Limited research manager, observed that the Covid-19 pandemic elevated credit risk and banks’ response by instituting strict lending policies as the economy is recovering have impacted the provisional losses of banks.

“The rise in private sector credit can be an indication that economic activity is slowly picking up following a serious global economic slowdown due to the Covid-1919 pandemic and demand for credit is growing,” he said.

Meanwhile, private sector credit expanded with an annual growth rate of 27 percent in June 2021 compared to a growth of 20.7 percent recorded in the preceding month and 12.1 percent registered in a corresponding month in 2020.

On a monthly basis, private sector credit increased by K37.6 billion to K776.2 billion in June 2021.

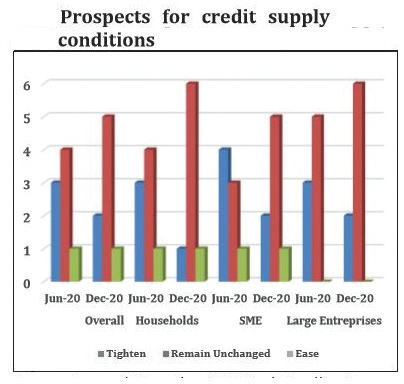

In its recent report, RBM indicated that credit standards and conditions for approval of loans and credit lines for most banks remained tight.

This outcome reflected banks’ efforts to remain proactive in credit risk management amid the Covid-19 pandemic and supporting creditworthy customers significantly affected by the pandemic.

Meanwhile, bad loans in the banking system increased to K44.1 billion as at end October 2020 from K43 billion in June 2020.