K3 trillion question!

From 2011, government has spent K3 trillion without being externally audited and devoid of parliamentary scrutiny of its audited annual accounts, it has been established.

The period without the annual audits—a crucial part of the financial reporting process—covers most of the era in which a PricewaterhouseCoopers (PwC) report last year said K577 billion in public funds could not be accounted for between 2009 and December 31 2014.

The absence of the Auditor General’s (AG) annual audit reports has alarmed the Institute of Chartered Accountants in Malawi (Icam) and corporate governance expert Anthony Mukumbwa.

The experts say the lack of AG’s annual audits further compromises the integrity of public finances already on trial following Cashgate—the systematic plunder of public funds now crippling government through the multi-billion kwacha heists and resultant direct budgetary support freeze by donors angry at the blatant fiscal sleaze.

One of the major causes of the AG’s report blackout—according to information from Treasury, the National Audit Office (NAO) and well-placed sources—is the delay by the Ministry of Finance, Economic Planning and Development in submitting consolidated annual accounts to the supreme audit institution.

Section 83 of the Public Finance Management Act (PFMA) stipulates that the Secretary to the Treasury shall, as soon as practicable, but not later than 31 October of each year, send to the Auditor General the financial statements of that year.

Yet, for example, it was only sometime last year that Treasury submitted draft financial statements to the AG for periods up to 2013/14.

The AG has only managed to finalise and submit to Parliament through the Minister of Finance the 2011/12 accounts, but the House is yet to discuss, said NAO.

NAO notes that the 2011/12 report was on the Order Paper of December 4 2015 of the 46thSession of Parliament ready for tabling and “Parliament Secretariat can best explain as to why the report was not tabled.”

The Nation’s review of the present order paper shows that the report is not on the agenda of the current sitting, which ends today.

By close of business yesterday, Parliament had not responded to why the 2011/12 audit report has not been tabled in the House.

Last month, in a response to a questionnaire for this story, Treasury said it would also submit to the AG draft financial statements for the 2014/15 fiscal year “within the month of February 2016”.

It was not immediately clear yesterday whether it was submitted as planned.

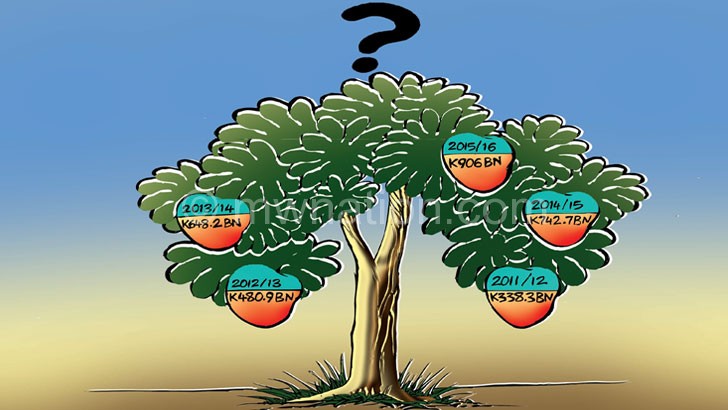

Since 2011, government has spent K338.3 billion (2011/12), K480.9 billion (2012/13), K648.2 billion (2013/14), K742.7 billion (2014/15) and is projected to spend K906 billion in 2015/16—bringing total expenditure to around K3.1 trillion to date.

In its response, Treasury blamed decentralisation of annual reports to ministries, departments and agencies (MDAs) and the partial implementation of the Integrated Public Finance Management System (Ifmis) as chief reasons for delays to submit financial statements to the AG.

It explained that beginning from 2011/12 fiscal year, government decentralised the preparation of vote financial statements to MDAs in line with PFMA and international best practice.

What this means, said Treasury, is that the Accountant General (AcG) awaits MDAs to prepare their financial statements before consolidating them into accounts that are presented before Parliament.

“This process of decentralisation of the preparation of financial statements brought its own challenge in the sense that consolidated financial statements could not be completed until all MDAs had finalised their own financial statements,” said Treasury.

On Ifmis, Treasury said the system was not comprehensive as several transactions were done outside it, which meant a lot of time was spent on the process of preparing the financial statements by MDAs at year end.

But it said: “Government has worked on the challenge of the many transactions that were outside Ifmis. Similarly, the new requirement by Treasury that demands monthly reports from MDAs, has led to a situation where most of them are always current and accordingly, would not require too much time to finalise the preparation of financial statements at year end.”

But blaming the delays on decentralisation of financial statements to MDAs and Ifmis could be problematic given that the problem of audit backlogs is an old one and pre-dates both the said devolution and Ifmis.

On its part, NAO said preparation of the reports submitted to Parliament is dependent on the input from other key stakeholders, including the AcG and Secretary to the Treasury.

The Public Audit Act requires the Auditor General to submit to the President and to the Speaker of the National Assembly the audits by December 31 of each year.

“Currently, we are processing the Auditor General’s reports for the years ended 30th June 2013 and 2014 based on the financial statements provided by Accountant General and the reports will be completed soon. It is our hope that the Auditor General’s Report for the year ended 30th June 2013 shall be ready for submission and tabling in the next budget session of Parliament,” said NAO spokesperson Lawrence Chinkhuntha in a response to a questionnaire.

But while Treasury’s delays to submit reports is one of the chief reasons for the holdup of audited accounts, NAO too has a litany of issues it says hindered timely consolidation and submission of the reports to Parliament through the minister.

Chinkhuntha said NAO delayed to produce audited reports because of Cashgate, which forced it to abandon some of its routine work to supervise the Baker Tilly work that revealed that around K24 billion may have been stolen between April and September 2013.

He said NAO also had to supervise the PwC data analysis and reconstruction of the government cashbook assignment that revealed the K577 billion scams.

Another reason for the delays, said Chinkhuntha, was that effective July 2013, the traditional way of auditing Consolidated Appropriation Accounts—which are financial statements prepared by the AcG consolidating financial statements only for all MDAs, changed to a new method whereby each MDA prepares its financial statements.

He said each of these have to be audited independently and issued with Auditor General’s opinion before consolidation takes place and the consolidated financial statements are issued.