New Reserve Bank of Malawi (RBM) data shows that women continue to be disadvantaged in digital financial services access.

If left unchecked, the trend, according to the central bank and industry insiders, could derail the country from achieving meaningful financial inclusion.

According to RBM December 2021 National Payments Systems (NPS) report, though traffic in electronic payment channels is rising, the retail payments segment continues to face challenges such as low participation of women in mobile money services.

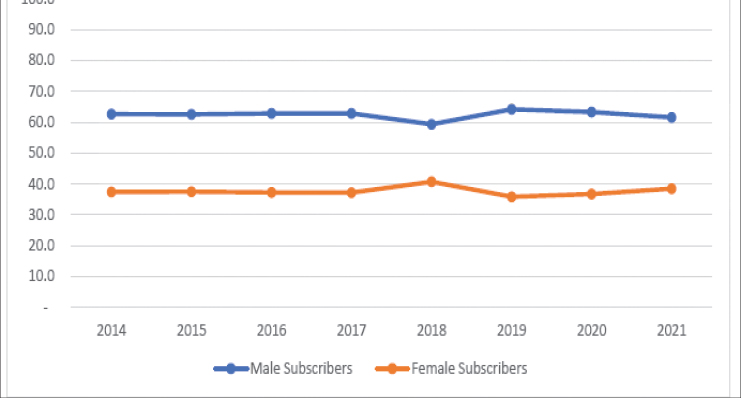

The report shows that although registered mobile money subscribers rose by 40.6 percent in 2021 compared to 2020, the gender gap remained wide at above 20 percent.

Reads the report in part: “The gender imbalance continues to be heavily skewed towards males as women only constitute 38.4 percent of the total subscriber base.

“The large gender gap is a cause for concern as it shows that women, who constitute the majority of the country’s population, are left behind in usage of mobile money services.”

In an interview on Wednesday, ICT Association of Malawi president Bram Fudzulani said the trend is a major problem which cannot be resolved if stakeholders continue working in isolation in their quest to achieve gender equality.

He said: “We need concerted efforts to address this gap. An organisation should not go in the rural area and only tackle women empowerment issues that leave out digital financial awareness which have proved to even empower women more when they are made aware of their power and usage.

“Our women inclusion efforts will not be meaningful if we leave out ICT and digital financial mass literacy, especially to the underprivileged communities.”

RBM figures further indicate that digital services usage has largely been limited to a few types of transactions among those available on the platforms.

The report also shows that geographical distribution of the agents remains a challenge as the majority of them are located in urban and semi-urban areas, with rural areas having fewer numbers to serve the huge population.

Consumers Association of Malawi (Cama) executive director linked the utilisation of digital financial services to the high illiteracy levels coupled with high transaction fees and security lapses as limiting factors to the full utilisation of digital financial services.

“What has been observed on these platforms is most people are unaware of the same especially the women who are naturally not as inquisitive as men but also there are issues of costs and that not much has been done to create confidence among traders and consumers on usage,” he said.